The current bull market in stocks is old by bull standards. It started in early 2009 when Ben Bernanke’s Fed staged a coup, assumed command of the US economy, and by default, the government. After all, they are following the strategy of controlling the money supply and therefore the government of a nation. The central bankers have initiated several quantitative easing periods, reduced interest rates at their bank to zero (thus affecting all interest rate coupons downstream), participated in multiple efforts to steal money from citizens and reward it to corrupt, fraudulent, bankrupt banker friends, and they continue to manipulate asset prices through action and rhetoric. The result has been a bull market in stock prices. That makes the idiots of the world believe in the ‘economic recovery’.

Where are we now in October of 2016?

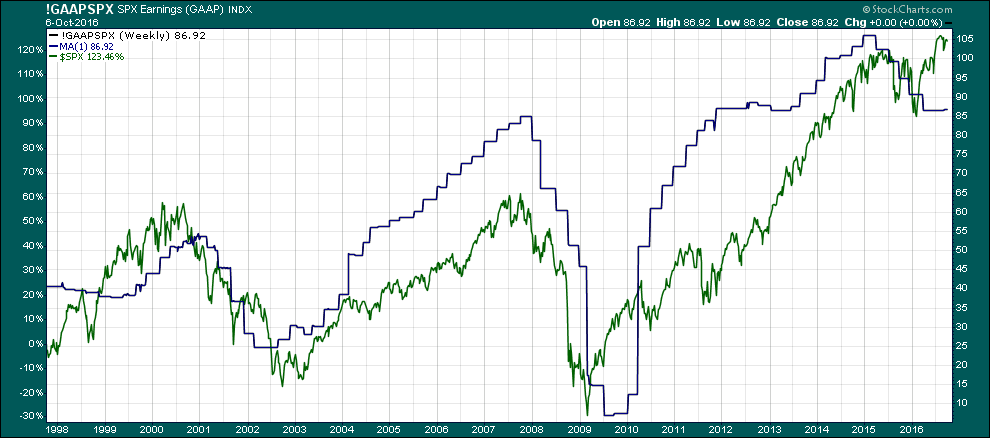

In one chart, we can see the artificial nature of the bullish trend. The chart at the end of this article is a 20-year look at the S&P 500 in green and S&P earnings in blue.

The first earnings decline, or recession, was a result of Alan Greenspan’s idiocy at the Fed. His low interest rates led to the tech bubble. The tech bubble burst, Greenspan raised rates, and corporate earnings followed stock prices lower. As is the case for military industrial powers, the solution to an economic recession was to implode a couple of buildings, frame a patsy, lie about the event, and foment enough fear in the populace to launch military invasions of numerous countries. Military conquests always give the false impression of an improving economy due to the war effort spending.

Most importantly, the dead economy and the inability for bankers to make money gave rise to the derivatives era. Companies could issue and buy derivatives at will and make up any price they wanted to make the accounting look good. I call this the ‘mark to fantasy’ period. Naturally, corporate earnings rose with derivative valuations.

Greenspan the Idiot was followed by Bernanke the Idiot who continued to raise interest rates until the war effort had run its course and the economy was again contracting. The Bush regime changed the accounting practices for derivatives so corporations had to account for derivatives as for what they could actually sell them. This was the ‘mark to market’ period. Corporate earnings collapsed with stock prices. This all makes sense so far.

Then, since the military had already invaded every nation void of central bankers and military spending could offer no more growth, the Bush regime reversed course and changed ‘mark to market’ accounting back to ‘mark to fantasy’. And just like that, corporate earnings improved immediately. By valuing derivatives at whatever price made the accounting look good, earnings led stock prices higher into our current bull trend.

Today stocks are trading at near all-time highs. But what about corporate earnings? Fourth quarter of 2016 is anticipated by all to be the sixth straight quarterly decline in corporate earnings. Yet, stock prices are still elevated to bubble territory never before seen. It is also worth noting that in real 1930 dollar valuation, corporate earning are less than they were in 1929. This is the result of the Fed’s destruction of the dollar’s value.

To justify stock prices, earnings need to begin another period of growth. How likely is that? Or, to justify the decline in corporate earnings, stock prices need to fall. How likely is that given that the Fed’s sole mission is to support stock prices and by default, their bankster friends?

Given that earnings are almost back down to where they were in 2008, should stock prices mirror 2008 levels we can reason that stock prices could, and should, fall some 50% from current levels.

Given that corporations have used zero interest rates to buy back record levels of stock just to manipulate prices higher, we can reason that this effort is about to fail to keep the bubble intact.

However, given that the Fed is still in business, we should not expect a meaningful decline in stock prices. The Fed will simply not allow that to happen. Yes, they are already talking about ‘buying stocks on a consistent basis’ to keep the bubble elevated. So, corporate earnings will continue to ebb while stock prices will continue higher. Yellen the Idiot will not be content until stock valuations are more over-valued than ever before! Investors must hold their noses and close their eyes while bidding up stock prices.

What should the average investor do?

Recent government regulations will make it harder than ever for investors to find a true advisor. For example, I am not a fan of annuities but in some cases they may be appropriate. As an independent advisor, I only recommend commission-free annuities. There are only two of them that I know of. Since they don’t pay agents commission, the only way for an advisor to make money on them is to charge a very small advisory fee. As a bonus, these two annuities actually offer sub-accounts that can take advantage of a falling stock index should that ever be the case again. Don’t expect these no-load annuities to be offered by most agents, however. The companies that offer these annuities don’t even have sales people in the company to push the product. That’s why most people have never heard of this idea. If investors want the truth, give me a call.

In the meantime, look at the chart below. Falling earnings and rising stock prices cannot be a trend forever. We all must decide at some point whether it is more likely for stock prices to fall or it is more likely for corporate earnings to somehow begin to grow again. The chart seems to indicate that the current bull market is really just B.S.

S&P earnings in blue, S&P 500 in green over 20 years.

Chart courtesy stockcharts.com

Disclaimer: The views discussed in this article are solely the opinion of the writer and have been presented for educational purposes. They are not meant to serve as individual investment advice and should not be taken as such. This is not a solicitation to buy or sell anything. Readers should consult their registered financial representative to determine the suitability of any investment strategies undertaken or implemented. BMF Investments, Inc. assumes no liability nor credit for any actions taken based on this article.

No comments:

Post a Comment