Every now and then, fantasy and lies are dissolved by the truth. The truth cannot be denied. It cannot be misinterpreted. It cannot be distorted. When accepted, these points in time are known as a ‘come to Jesus’ moment. Only the truth matters. This past week, August 8, 2011 thru August 12, 2011, was a come to Jesus moment for the stock market.

For the first time in history, the Dow experienced four consecutive days where the closing price was 400 points higher or lower than the previous closing price. The major US indices lapsed into confirmed corrections and threatened to sink into bear market levels. At the end of the week, the indices were down a bit over 1.5%. That drop masks the incredible volatility with the Dow dropping 5.5% on Monday, rising 4% on Tuesday, dropping 4.6% on Wednesday, rising 3.9% on Thursday, and rising 1.1% on Friday. Tuesday’s rise was all due to a 600-point rally in the last hour of trading orchestrated no doubt by the Plunge Protection Team. Volume was similar to the March of 2009 PPT move. Where did all this volatility come from?

Let’s embrace the truth with one example.

The current regime seems to think the US debt problem can be cured by increasing the taxes on the ‘fat cats’. The truth is the fat cats already pay most of the taxes. The debt has ballooned because of fantasy thinking, lies, and regime incompetence. Consider a few companies that the regime operates.

Fannie Mae lost $5.1 billion in Q2 but issued $2.3 billion in dividend payments to the Treasury. How ridiculous is that?

The Post Office lost $3 billion in Q2 2011 and can’t make their $5 billion mandated pension funding payment to the Federal Employee Retirement System.

Amtrak lost $1 billion (2010).

Aside from the $100 billion or so already ‘invested’ in Fannie and Freddie, let’s take the $5 billion in quarterly losses and multiply by four quarters. Let’s do the same for the Post Office. Now we have annualized projected losses of $32 billion plus Amtrak’s $1 billion to bring us to $33 billion total. The top 10% of income earners (about 14,000,000 taxpayers earning in excess of $113,000 AGI) pay about 70% of all taxes (IRS data). Since the US Treasury will have to write a check to these money losing government institutions, the taxpayers essentially pay for all these government subsidized loses. So, if the ‘fat cats’ have to pay for 70% of these losses, $33,000,000,000 times 70% equals $23,100,000,000. Now, $23,100,000,000 divided by 14,000,000 (‘fat cats’) equals $1,643 per ‘fat cat’. The portion of the tax bill for the ‘non-fat cats’ (126,000,000 taxpayers divided into $9,900,000,000) is $79 per taxpayer. Aren’t the fat cats paying their ‘fair share’?

‘Fat cats’ already pay other taxes that ‘skinny cats’ don’t. The stock market is the capital structure that allows publicly traded businesses to function, grow, and produce jobs. Fat cats own almost all the stock and therefore pay capital gains taxes as well as dividend taxes. Skinny cats pay neither but find employment from the effort of fat cats.

‘Fat cats’ own the real estate where the skinny cats work and rent shelter. Yes, there is some pass through but the fat cats pay the real estate taxes as well as sales taxes when they sell such properties.

‘Fat cats’ pay the employer half of the Medicare/Medicaid taxes. They pay business taxes and licenses. They pay the myriad of government regulation fees. They run all the risk of government seizure and closure for failure to comply with any of the litany of business requirements imposed by such government. The skinny cats are absolved of all such responsibility and taxation.

Again, there is some degree of pass-through as the wealthy that own the businesses simply pass on extra costs and taxes to the consumer and employees. To that argument, raising taxes on the ‘fat cats’ is really a tax increase on the skinny cats. The other argument is that the fat cats already pay a great percentage of the taxes in the US already. Many of these taxes take a form other than federal income tax.

So the debate on how to solve the US debt addiction has finally burst into the public conscience. The previous example of taxation is one variable. But for our purposes, how has the come to Jesus moment on US debt affected the stock market? This past week reflects the realization of the truth.

Friday, 8/12/2011 - Stock indices have entered an official correction. There has been talk of recession in the air. Europe has been a basket case. Worse, the stock market has been fading. What to do, what to do? Just in time for some cheery news, the DOPE (Department of Pathological Embellishment better known as the Commerce Department) said retail sales for July had gained the most since Spring. This is one day after the Labor Department said new applications for unemployment had fallen below the 400,000 level. See - the economy is improving! It is! Really it is! The government said so! It is improving, damn it! Let’s put the crack pipe down for a moment and examine a few details.

According to even government figures, only 58% of working age Americans have a job right now. That means that 42% of working age Americans are unemployed. If even half of those unfortunate people are actually looking for work, the real unemployment number should be higher than 20%. Yes, unemployment benefits do run out over time so many people drop off the rolls each month. What really matters in any society is the ratio of productive adults to non-productive adults. The many can keep up the few but the few cannot keep up the many. We do know that in spite of this wondrous trend in falling unemployment claims, the US has rising poverty and food stamp dependent populations. Maybe the unemployment claims are falling because a good many of the unfortunately unemployed are selling crack to the government departments that compile the happy news!

Retail sales rose in July. Really? We must remember that the same government department that compiles retail sales also compiles GDP. That would be the DOPE. Remember first quarter GDP? The DOPE had to revise down the first reported 1.4% growth rate to .3%. How accurate do we really expect any of their numbers to be? We should also remember that the GDP downward revision came before the stock market buckled into a correction. Everything was fine so the DOPE could give us some bad news. Now the stock market has crashed and the DOPE is feeding us some unexpectedly good news. What a coincidence. Well, let’s look at the numbers.

According to the retail sales report, the past three months have seen an 8.2% rise over the same period last year. Swell. However, the biggest increase came from gas stations. Yes, we all know that the price of gas is up, up, up! The extra spending on gasoline should logically have left consumers with less to spend on other stuff. But we are not dealing with logic here. The government needs a stock rally and they need some good news to feed to traders. According to DOPE, retail sales still rose even with gasoline sales stripped out. Sales of electronics and appliances rose 1.4%. However, sales at department stores and building-material suppliers fell. Again, with the crack pipe extinguished, it would seem pretty logical that electronics and appliances are sold at department stores and building-material stores. Where then, would all the sales come from in electronics and appliances if they are not purchased at departments stores and building-materials stores?

Further, the University of Michigan/Thomson Reuters index reported that consumer sentiment had dropped in August to 54.9 - the lowest reading since 1980. Let’s review. We have high unemployment, very low economic growth, an inept government, a current stock market correction underway, a credit downgrade by Standard & Poor’s, an economic growth expectation downgrade by the Federal Reserve, and yet the strongest consumer spending number in months. Yeah, it makes sense to me!

And yes, there is more bad news today. The Greek GDP for Q2 has come in at minus 6.9%. With the economy contracting sharply, where will Greece find the extra money to pay for their latest bailout package from the ECB? Some of their neighbors are laboring as well. Italy and Spain have descended into desperation mode as they joined France and Belgium in banning short selling of bank stocks. Selling short is selling shares that are not owned in a bet that the share price will decline at which point the buy-to-cover is made. Banning short selling just means that the regulators are trying to rig the market for gains only. It means the regulators don’t trust the ‘market’ to discover truth and reality in terms of stock prices. I always thought stock prices were supposed to reflect truth and reality?

Maybe they finally are reflecting truth. Maybe this past week was a come to Jesus moment for stocks. Maybe investors have discovered that the government does not have an economic solution that works. Maybe the Federal Reserve is clueless. Maybe the green shoots were just weeds. What’s going to happen in the coming weeks? Maybe we should look at Tuesday, August 9, 2011.

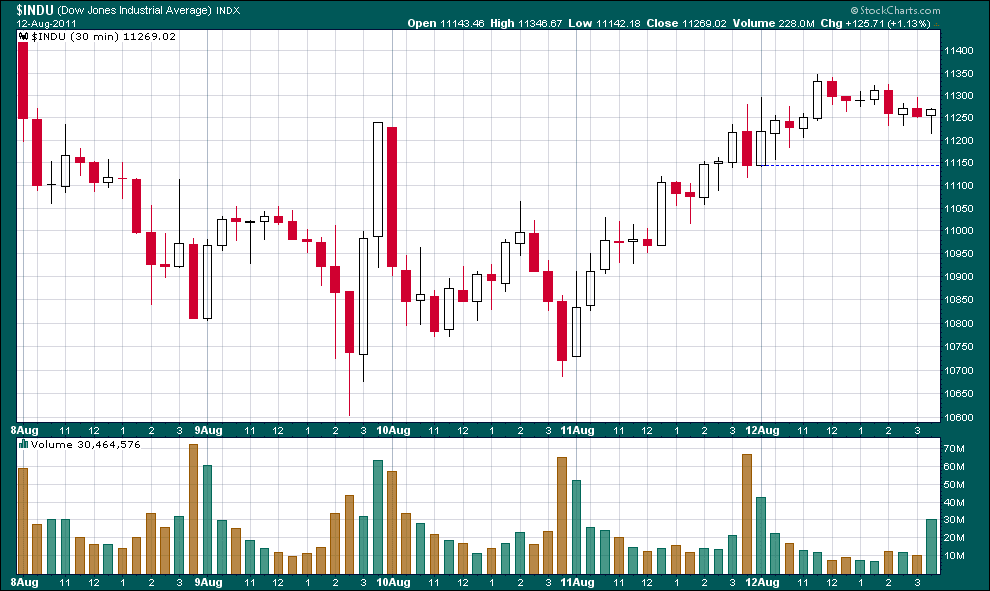

The chart below is the incredible week of August 8 -12, 2011 with 30-minute candles. On Tuesday, the Fed met and promised to keep the Fed Funds target rate at zero forever and ever. Actually I think they babbled something about mid-2013 but I think we all now understand that the idea of raising interest rates is like making plans for a midnight snack on the Titanic. That news prompted a major rally in Treasuries and a resumption of selling in stocks. The Dow was down 200 points at about 3:00 PM. That prompted a major PPT move that drove the Dow 600 points straight up in a hour! Why can‘t the Fed let investors discover stock price valuations? What are they afraid of - the truth? Stocks need to find a bottom. Will the Fed let them?

DJIA 1 Week: 08/08/2011 - 08/12/2011 30-minute bars

Chart courtesy StockCharts.com

Disclaimer: The views discussed in this article are solely the opinion of the writer and have been presented for educational purposes. They are not meant to serve as individual investment advice and should not be taken as such. This is not a solicitation to buy or sell anything. Readers should consult their registered financial representative to determine the suitability of any investment strategies undertaken or implemented. BMF Investments, Inc. assumes no liability nor credit for any actions taken based on this article. Advisory services offered through BMF Investments, Inc.